Article 4: Interest Reconsidered

Series: Money, Inflation and Interest Reconsidered

Introduction

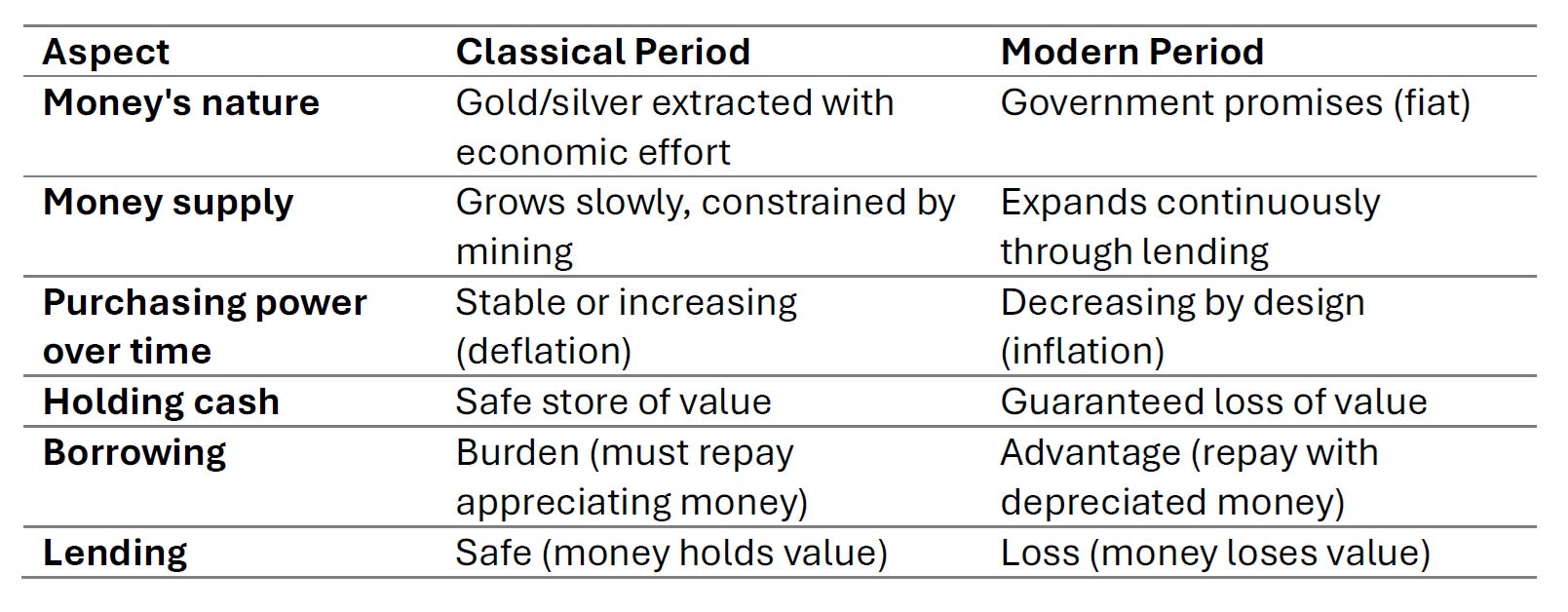

Muslims accept that Riba is detestable and impermissible. Most Muslims accept legal rulings that interest on money saved in a bank is Riba based on rulings reached by jurists in the foundational years of Islam. However, the nature of money has fundamentally changed since those rulings were developed. Classical Islamic jurists operated under gold and silver standards where money naturally held or gained value over time. Today’s fiat money is designed to lose value.

Islamic legal principles demand that we consider essence over names, and meanings over words. The scholars established that al-ibratu lil-ma’aani la lil-alfaaDH (consideration is given to meanings, not words) and al-i’tibaaru bil-maahiyah la bil-ism (consideration is for the essence, not the name). Yet we apply rulings about money from the classical texts to something we call “money” today that is essentially different from what the early scholars understood and assumed by that term.

Since like me, you probably have a savings bank account, that accrues interest without your consent, you will be interested in this series. This series aims to inform you on how the “money” is created today, and how it works, then invite us to reconsider under what circumstances is interest on saved money Riba. I’m sure you will learn something even if you don’t have a savings bank account. Now we arrive at the central question: how should we understand monetary interest when the monetary context has completely reversed?

What We Now Know

From the previous articles, we learned:

Today’s money is created through lending and is inherently inflationary by design

The fiat system systematically transfers wealth from savers to borrowers and from ordinary people to those connected to money creation

Muslims who avoid interest-based finance often find themselves on the exploited side of this transfer

Classical Islamic jurisprudence developed under gold and silver standards that were predominantly deflationary

Under deflationary conditions, prohibiting interest protected borrowers from compound exploitation

The monetary system has completely reversed: from money that held or gained value to money designed to lose value

The question before us is whether rulings developed for one monetary reality apply unchanged to a completely different monetary reality.

What We Will Learn

In this article, we will learn1:

How inflation reverses the moral logic of lending transactions

Who becomes the exploited party when money loses value by design

A framework for distinguishing between compensation for monetary loss and actual exploitation

How to think about intertest in terms of real value rather than nominal numbers

What this analysis means - and does not mean - for Islamic finance and individual Muslims

Key Terms

Real interest rate: The nominal interest rate minus the inflation rate. If a loan charges 7% interest and inflation is 5%, the real interest rate is 2%.

Economic neutrality: A transaction where neither party gains nor loses real purchasing power from the monetary system itself.

Nominal value: The number written on money or in a contract.

Real value: What that nominal value actually purchases in goods and services.

The Great Reversal

Everything we have learned points to one unavoidable conclusion: the monetary system has undergone a complete reversal from the world the classical scholars knew.

This is not a minor adjustment or a modest difference in degree. It is a complete inversion of the fundamental dynamics of money.

How Inflation Reverses the Moral Logic

Let us trace through a lending transaction today to see how the moral dynamics have changed.

Loan in Today’s System

Imagine you lend someone ₦1,000,000 today in an economy with 10% annual inflation. You agree that they will repay ₦1,000,000 in one year, with no interest; following the traditional prohibition of Riba.

One year later, the borrower repays exactly ₦1,000,000. The contract has been honoured. No interest has been charged or paid.

But what has actually happened in terms of real value?

That ₦1,000,000, due to 10% inflation, now purchases only what ₦900,000 could have purchased when you made the loan. You lent purchasing power equivalent to 1,000,000 “units of value” and received back only 900,000 “units of value.”

Where did the missing 100,000 “units of value” go? To the borrower. They received the full use of 1,000,000 units of value for a year and returned only 900,000 units of value. The monetary system - inflation built into fiat currency - transferred wealth from you to them.

This Is Not Market Risk

Someone might object: “But lenders have always faced risks. The borrower might default. The investment might fail. That’s just the nature of lending.”

This objection misunderstands the situation. The wealth transfer we’re describing is not a risk; it’s near certainty. Inflation is built into fiat monetary policy by design. Central banks explicitly target positive inflation rates. The outcome is not uncertain; it is guaranteed.

When you lend money in a fiat system expecting only nominal repayment, you are not taking a risk. You are accepting a certain loss. The only question is how much you will lose, not whether you will lose.

The Systematic Nature of the Transfer

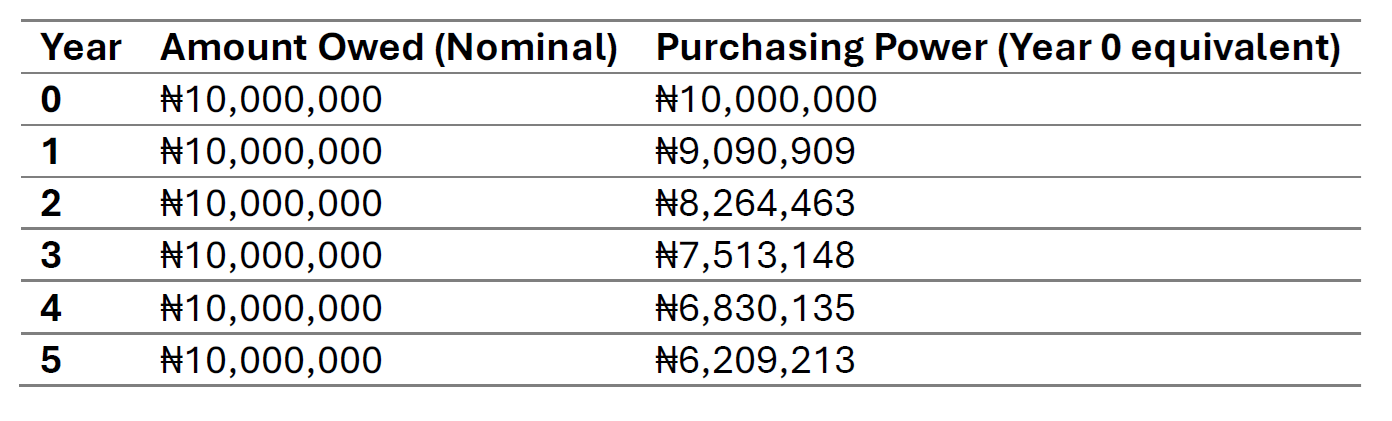

Let us extend the example. You lend ₦10,000,000 over five years with 10% annual inflation.

After five years, the borrower returns ₦10,000,000; the exact amount borrowed, no interest charged. But that ₦10,000,000 now purchases only what ₦6,209,213 could have purchased when the loan was made. The lender has lost nearly 38% of their wealth, not through any failed investment or business risk, but simply through the mechanics of fiat money.

Meanwhile, the borrower has enjoyed the use of the full ₦10,000,000 for five years and returned less than two-thirds of its value. The monetary system handed them a gift worth nearly ₦3,800,000 in real terms.

The Inversion of Predator and Prey

Under the deflationary standard, the dynamics were clear:

The borrower was vulnerable; needing money, facing repayment with potentially appreciating currency

The lender held power; possessing money that held its value, able to demand interest

Interest tipped the balance further toward the lender, potentially trapping the borrower

The prohibition of interest protected the vulnerable borrower from exploitation

Under the inflationary standard, these dynamics reverse:

The borrower holds a structural advantage; they will repay with depreciated currency

The lender is vulnerable; their money loses value every day it remains loaned out

Demanding only nominal repayment already disadvantages the lender

The prohibition of interest now protects the party who already holds the advantage

This is not a minor adjustment. The hunter has become the hunted. The protected has become the exploiter. The exploiter has become the victim.

The Scale Balanced and Unbalanced

Think of a scale representing the balance between borrower and lender.

Under the gold standard, the scale naturally sat level or tipped slightly toward the lender (since their money held or gained value). Allowing interest tipped it further, potentially crushing the borrower. Prohibiting interest kept the scale roughly balanced; neither party exploited by the monetary system itself.

Under fiat money, the scale already tips toward the borrower before any interest is considered. Their money depreciates; they benefit automatically. Prohibiting interest does not restore balance; it tips the scale further in the direction it was already leaning. The “protection” now harms the party who is already disadvantaged.

Distinguishing Compensation from Exploitation

If this analysis is correct, we need a framework for distinguishing between two very different things:

Compensation for monetary debasement: Payment that simply restores the lender to the same purchasing power they lent

Actual exploitation: Payment that transfers real wealth from borrower to lender

The Scenarios

Consider three scenarios, all with 5% annual inflation:

Scenario A: Interest Rate = 0% The lender loses 5% purchasing power per year. Wealth flows from lender to borrower through inflation. The borrower gains at the lender’s expense, not through any productive activity but simply through monetary mechanics. The lender suffers injustice.

Scenario B: Interest Rate = 5% The lender receives back the same purchasing power they lent. The interest payment exactly offsets inflation. No wealth transfer occurs in either direction. Neither party is exploited. The transaction is economically neutral.

Scenario C: Interest Rate = 10% The lender receives back more purchasing power than they lent; 5% more after accounting for inflation. This extra 5% represents a real transfer from borrower to lender. This is the classical case of exploitation through lending.

A Refined Definition

These scenarios suggests a more precise understanding:

Riba to a lender, within a monetary system whose engine is Riba, occurs when the interest rate exceeds the inflation rate. The amount of Riba is the positive difference between them.

If inflation is 5% and interest charged is 10%, then the extra 5% constitutes Riba while the first 5% represents mere compensation for monetary debasement; restoring the lender to their original position rather than enriching them.

If inflation is 5% and interest charged is 5%, no Riba occurs. The transaction is neutral.

If inflation is 5% and interest charged is 0%, the borrower receives a wealth transfer from the lender. This is not Riba in the classical sense, but it is injustice flowing in the opposite direction.

Substance Over Form

The Islamic legal tradition has always emphasized substance over form via sayings like “consideration is given to meanings, not words” and “consideration is for the essence, not the name.”

A contract that uses the word “sale” but functions as a loan is judged as a loan. A transaction that avoids the word “interest” but delivers the same economic effect is judged by its effect. Labels do not determine reality; substance does.

Applying this principle:

A loan at 0% interest in an inflationary environment is not, in substance, a neutral transaction. It is a transaction that transfers wealth from lender to borrower through monetary manipulation external to the contract itself.

A loan at the inflation rate is, in substance, a neutral transaction. The lender receives back what they lent in terms of actual purchasing power. Neither party exploits the other.

A loan above the inflation rate is, in substance, an exploitative transaction to the extent it exceeds inflation. The lender extracts real wealth from the borrower.

If we focus on forms - on the word “interest” appearing or not appearing - we may prohibit neutral transactions while permitting exploitative ones (through inflation). If we focus on substance - on whether real wealth transfers unjustly - we can identify actual exploitation regardless of what the paperwork says.

Addressing Potential Objections

This analysis will face several objections. Let us address some of them.

Objection 1: “This opens the door to interest-based banking.”

This is the most common concern, and it deserves serious engagement.

The argument presented here does not mean:

All conventional banking is now halal

Compound interest is acceptable

Banks can charge whatever they want and call it “inflation adjustment”

Other Islamic requirements for ethical finance can be ignored

Speculation, gharar, or other prohibited elements become permitted

The wealthy exploiting the poor through lending is now acceptable

What the argument does mean:

A lender asking to receive back the same purchasing power they lent is not exploiting the borrower

The question of exploitation begins only after inflation is accounted for

Charging no interest or less than inflation is still virtuous, but not because the lender is avoiding Riba, but because the lender is willingly transferring wealth to the borrower; that is Sadaqa

Islamic finance should focus on preventing actual exploitation rather than policing nominal numbers

We may need a better alternative name to banking under Islamic finance because “non-interest banking” may not work anymore

The door being opened is not to exploitation but to accuracy. We are trying to identify where exploitation actually occurs, not to permit exploitation.

Objection 2: “Inflation is difficult to measure accurately.”

This is true. Official inflation statistics like the Consumer Price Index (CPI) are imperfect, subject to manipulation, and may not reflect individual circumstances. The basket of goods used to calculate CPI is updated over time, and different people experience different rates of price increase depending on what they buy.

However, this difficulty does not invalidate the principle. Islamic jurisprudence routinely requires scholars to make practical judgments about economic realities, like evaluating whether a sale involves excessive risk (gharar). The difficulty of precise measurement does not mean we should ignore the phenomenon entirely. A rough adjustment for inflation, even if imperfect, is more just than no adjustment at all; which guarantees injustice to lenders.

Moreover, there are alternative ways to measure inflation, one of which is the growth in money supply. If the money supply grows by 15% but official inflation statistics (CPI) show only 5%, the discrepancy suggests the real loss of purchasing power may be closer to 15%, or at least in-between.

Objection 3: “The classical scholars knew what they were doing.”

Absolutely. The classical scholars were brilliant jurists whose reasoning was sound and whose moral concerns were valid. Nothing in this argument suggests they were wrong; we are more likely wrong.

They developed rulings fitted to their monetary reality. In a deflationary environment with gold and silver currency, prohibiting interest protected the vulnerable from exploitation. Their rulings were just.

The question is not whether the scholars were right in their context, but whether applying their rulings unchanged to a completely different context achieves the similar just outcomes.

We honour the scholars’ wisdom precisely by applying their principles to our reality after identifying what is similar and different between their context and our context, rather than assuming the two contexts are essentially the same.

Objection 4: “This is just making excuses for interest.”

First, not all interest is Riba, and not all Riba is interest. This objection assumes that any reconsideration of traditional rulings is motivated by desire to escape them. Traditional rulings on interest are not sacred, they were arrived at by effort of scholars who deeply understood their context, and so we should demand deep understanding of our monetary system before making decisions. This is not escaping traditional rulings; it is applying the process of the traditional rulings rather than its outcomes.

Many observant Muslims currently suffer losses under the fiat system precisely because they follow the outcomes of traditional rulings. They avoid interest-bearing accounts, so their savings erode. They avoid conventional mortgages, so they rent while landlords build equity. They avoid business financing, so they cannot expand while competitors leverage credit.

The current application of traditional rulings does not protect these Muslims from exploitation; it subjects them to exploitation by the monetary system while they believe they are being virtuous. However, virtue is both putting effort into not suffering loss, as well as not causing others to suffer loss (Q2:279).

If anything, this analysis seeks to genuinely protect Muslims from exploitation by helping them understand when exploitation begins in the financial system.

What This Means (and What It Does Not Mean)

Let us be very clear about the scope and limits of this analysis.

What This Analysis Suggests

Inflation-matching compensation is not Riba. Receiving payment that restores you to your original purchasing power is not exploitation. It is neutrality.

Real value matters, not nominal value. Focusing on whether a transaction charges “interest” while ignoring systematic wealth transfers through inflation misses the substance for the form.

The question of exploitation starts after inflation is accounted for. Once we’ve established economic neutrality, then we can ask whether additional charges constitute exploitation.

Current practice may inadvertently harm observant Muslims. By insisting on 0% nominal interest in an inflationary environment, we may be requiring Muslims to accept systematic exploitation while believing they are avoiding sin.

Islamic finance needs to address substance, not just form. Complex structures that technically avoid “interest” while operating in an inflationary system may be focusing on the wrong variable.

What This Analysis Does NOT Suggest

This is not a fatwa. This is an intellectual argument inviting scholarly reconsideration, not a religious ruling.

All conventional banking is not thereby halal. Conventional banking involves many elements beyond simple interest; compound interest, exploitative terms, speculation, lack of transparency. Addressing inflation does not address these other concerns.

High interest rates are not justified. Interest rates far exceeding inflation remain exploitative. A 25% interest rate in a 5% inflation environment includes 20% genuine extraction from the borrower.

Individual circumstances do not change. A poor person charged high interest by a wealthy lender remains an object of concern even if some portion represents inflation adjustment. The power dynamics and potential for exploitation remain.

The prohibition of Riba is not being challenged. The argument refines our understanding of what constitutes Riba under changed circumstances. It does not challenge the prohibition but seeks to apply it accurately.

Implications for Islamic Finance

If this analysis has merit, what might it mean for how Islamic finance operates?

This might mean:

Pricing products based on real rather than nominal returns

Explicitly accounting for inflation in determining fair compensation

Focusing on whether transactions genuinely avoid exploitation rather than whether they technically avoid “interest”

Developing products that actually protect their customers from the wealth-extracting effects of fiat money

What About Individual Muslims?

For an individual Muslim navigating the current system, this analysis suggests that keeping money in a 0% savings account while inflation runs at 10% is not religious virtue; it is accepting systematic wealth extraction while believing you are being righteous. The person who charges you nothing for inflation is losing, and you are gaining at their expense, though they may be happy to help. But do they know that they are giving you Sadaqa?

It suggests that the relevant question when evaluating financial products is not simply “is there interest?” but “what is the real transfer of wealth between the parties?”

These are questions for individuals to consider when engaging scholarly opinions, and for Islamic financial institutions to address thoughtfully.

Are These Recommendations New?

Whilst there may be some novelty to the analysis and argument presented in this series, the recommendations presented are generally not new. Contemporary Islamic scholars have been grappling with the implications of interest in fiat money for decades, and significant disagreement exists.

Some scholars maintain that the traditional rulings apply unchanged regardless of monetary conditions. In this view, interest is interest; any predetermined increase in a loan is Riba, full stop. The monetary system’s effects are external to the contract between borrower and lender, and Muslims must simply accept whatever losses inflation imposes as the cost of following the Shariah. Scholars in this camp often point to the explicit Quranic texts and argue that human reasoning cannot override clear prohibitions.

Other scholars have questioned whether rulings developed for commodity money can apply identically to fiat currency. They note that the classical jurists themselves distinguished between different types of money and recognized that legal rulings must account for underlying realities. Some have argued that fiat currency is not “money” in the classical legal sense at all, which would require rethinking numerous rulings beyond just Riba.

A middle position holds that while the prohibition of Riba remains absolute, its application requires understanding what constitutes Riba under changed circumstances. Scholars in this camp argue that the goal of the Shari’ah (Maqasid al-Shariah) should inform how we apply specific rulings, and that a mechanical application that produces injustice cannot be what God intended.

The debate remains unresolved, and this article does not claim to settle it, though it takes a position.

Beyond the Recommendations

The recommendations of this series are not as important as the analyses that support the recommendations. After all, scholars have discussed the concept of “indexation” for decades. The question of indexation asks: when the value of currency changes significantly between the time of borrowing and repayment, should the debt be adjusted to reflect this change? Should a borrower who took a loan when the currency was strong repay more nominal units when the currency has weakened, to ensure the lender receives equivalent real value?

Some scholars have permitted indexation in cases of severe currency depreciation, arguing that justice requires the borrower to return equivalent value, not merely equivalent numbers. Others have permitted pricing contracts in stable units of account (such as gold, or a basket of commodities) even when payment occurs in local currency.

That said, the understanding of how fiat money works, in contrast to how hard money works, is very useful in answering even bigger questions: are we stuck in the fiat monetary system in the future; are there sound money alternatives to the fiat system; how do we implement sound money if the alternatives are not feasible; how can waqf be sustained in a fiat system; how is Zakat affected by being in a fiat system; how should we save money in a fiat system; what harms of the financial market can be attributed to the fiat system?

Conclusion: Returning to First Principles

We began this series with a problem: most Muslims accept the dominant ruling applied on interest as Riba without understanding that the nature of money has fundamentally changed since those rulings were originally developed.

We have seen:

Fiat money is created through lending and is inherently inflationary

The fiat system systematically transfers wealth from savers to borrowers

Classical jurisprudence developed under completely different monetary conditions

The prohibition of interest made perfect moral sense under deflationary money

The monetary reversal inverts the dynamics the original prohibition addressed

The fundamental Islamic principle underlying the interest prohibition is preventing exploitation and ensuring justice in economic relationships; neither suffering loss nor causing others to suffer loss.

When the monetary system itself creates systematic wealth transfers, ignoring this reality does not preserve Islamic principles; it subverts it. Savers are exploited while believing they are being virtuous. Borrowers receive windfalls while believing they are following the rules.

The call of this analysis is not to abandon Islamic principles but to apply them accurately. Not to permit exploitation but to identify where exploitation actually occurs. Not to ignore the classical scholars’ output but to follow their reasoning process to circumstances they never faced.

Consideration is for the essence, not the name. What we call “money” today is not what the scholars meant by money. What we call “fair repayment” may not be fair at all. What we call “avoiding interest” may be accepting exploitation.

The essence matters more than the name. The meaning matters more than the words. And justice (real justice between the contracting parties) matters more than formal compliance with rules developed for a world that no longer exists.

This is an invitation to reconsider. The conversation is just beginning.

And beyond this conversation, there are many questions to explore.

This article concludes the series “Money, Inflation, and Interest Reconsidered.” The arguments presented are intended to stimulate scholarly discussion and individual reflection. May God guide us to truth and justice in all our affairs.

Sources: The main source of historical facts and economic concepts are from “The Fiat Standard: Debt Slavery Alternative to Human Civilization” by Saifedean Ammous. Another book consulted is “Debt: The First 5000 Years” by David Graeber. Given the distance between the two books on the political spectrum, the series ends up presenting concepts that sometimes don’t fit completely with either source. The concepts from Islamic jurisprudence are well known in the field and require no citation.

Audience and Style: The readership is for a general audience with about secondary school education and of no particular background. Consequently, the style is expansive with ample - and sometimes repetitive - explanation that may seem tedious to those familiar with much of the concepts. The reader is welcome to skim through parts elaborating on concepts already familiar. To make the arguments focused, nuance was applied only where justified, otherwise every sentence could be a digression.